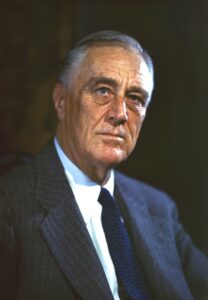

Democratic (socialist/fascist) de facto President Franklin Roosevelt, Esq., signs the Internal Revenue Act of 1942:

Decreasing the number of personal income tax brackets from 32 to 24;

Increasing the lowest personal rate on the first 2,000 “dollars” earned from 10% to 19%;

Increasing the number of corporate profits (income) tax brackets from 2 to 3;

Increasing the lowest corporate rate on the first 25,000 “dollars” earned from 30% to 34%;

Increasing the highest corporate rate on amounts earned over 25,000 “dollars” from 44% to 47% on amounts earned over 50,000 “dollars”;

The middle corporate rate is established at 53% on amounts between 25,000 and 50,000 “dollars”;

Replacing the 35% to 60% graduated tax on “excess” corporate profits with a flat rate of 90%”;

Maintaining the highest personal rate at 88%, but dropping the threshold from 500,000 to 200,000 “dollars”; and

Establishing a 5% “Victory Tax” on any personal “income” over 624 “dollars”—to be withheld from each paycheck, every payday.

NOTES:

The concept of payroll tax withholding for the Victory Tax was new to U.s. subject/enemy/citizens; they had already been subject to payroll tax withholding since the advent of Social Security seven years previous;

This is the further realization of plank number two of the Communist Manifesto by Karl Marx.